Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

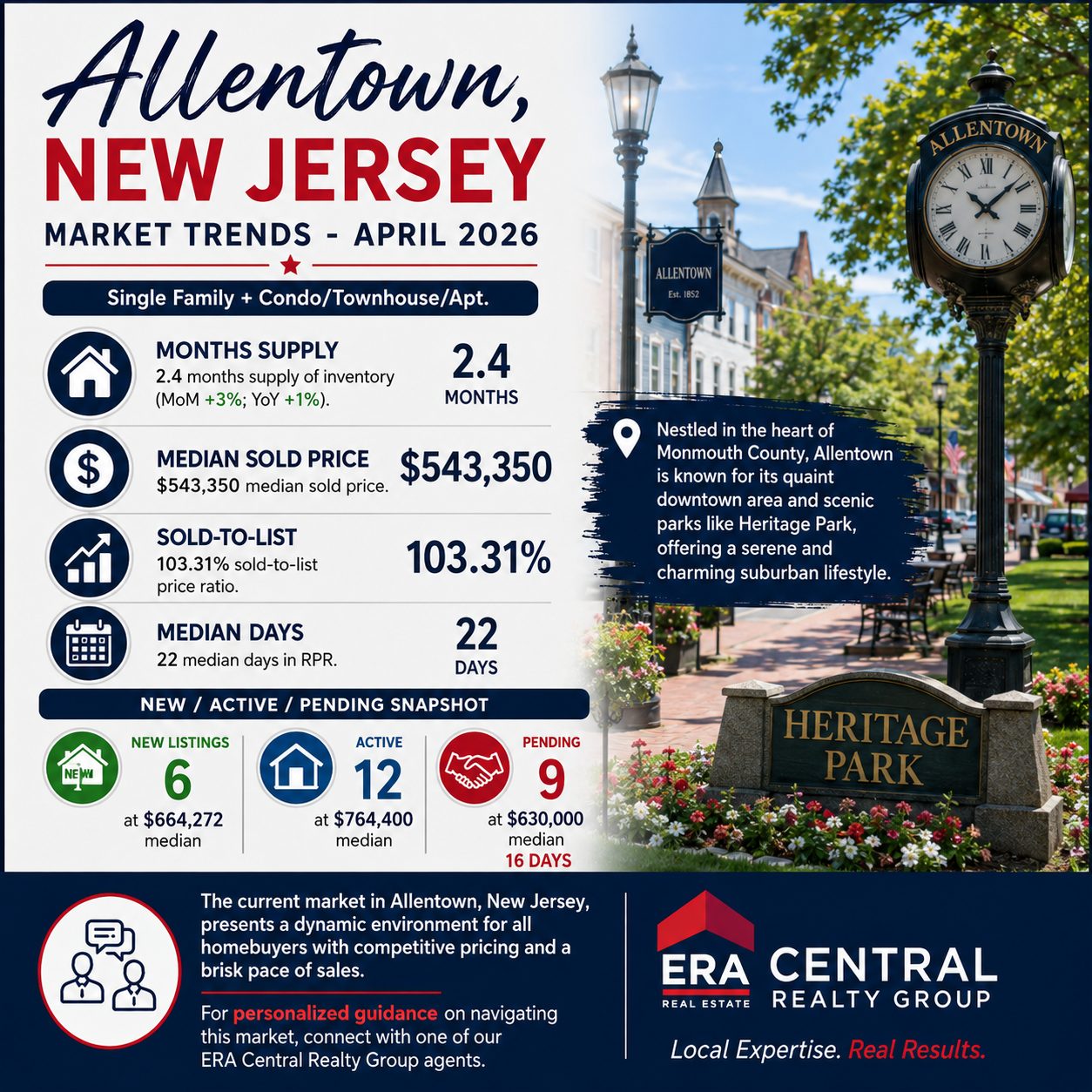

Welcome to Allentown, New Jersey, April 2026, Single Family + Condo/Townhouse/Apt.

Are prices rising?

Yes, the median list price for active listings is $764,400, while the median sold price is $543,350. This indicates a competitive market with a 103.31% sold-to-list price ratio.

How is the inventory looking?

The inventory is slightly increasing, with a 3% one-month change and a 1% change over the last twelve months, offering a 2.4 months’ supply of inventory.

What about new listings?

There are 6 new listings with a median list price of $664,272, which suggests that buyers have options but should act quickly due to the limited availability.

How quickly are homes selling?

Homes in Allentown spend a median of 22 days in RPR, with new pending listings averaging 16 days, reflecting a brisk market pace.

Allentown is known for its charming downtown and access to scenic parks, offering a quaint lifestyle with convenient commuting options. For personalized guidance in navigating the Allentown housing market, connect with one of our ERA Central Realty Group agents.