Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

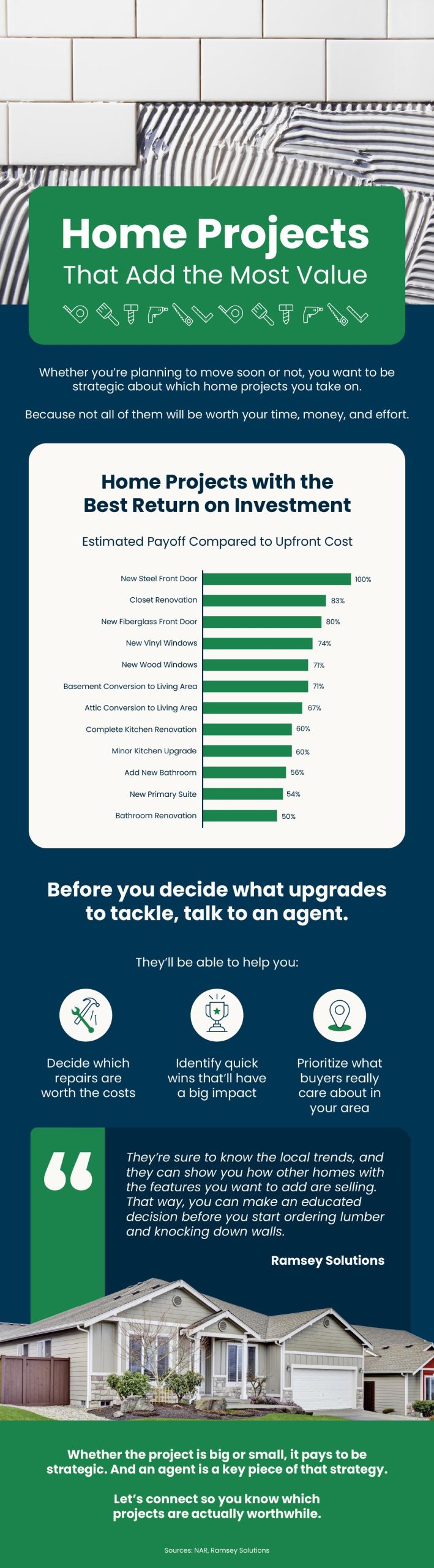

Home Projects That Add the Most Value

Some Highlights

- Whether you’re planning to move soon or not, you want to be strategic about which home projects you take on. Because not all of them will be worth it.

- Before you decide what upgrades to tackle, talk to an agent who knows what’s in demand in your area and where you’re most likely to recoup the costs.

- Connect with a local agent so you know which projects are actually worthwhile.

Is It Better To Rent or Buy a Home?

You’ve probably asked yourself lately: Is it even worth trying to buy a home right now?

With high home prices and stubborn mortgage rates, renting can seem like the safer choice right now. Or maybe your only choice. That’s a very real feeling. And perhaps buying today isn’t your best move; it’s not for everyone right away. You should only buy a home when you’re ready and able to do it, and if the timing is right for you.

But here’s the thing you need to know about renting.

While it may feel like a safer bet today – and in some areas might even be less expensive month-to-month than owning – it can really cost you more over time.

In fact, a recent Bank of America survey found that 70% of aspiring homeowners worry about what long-term renting means for their future. And they’re not wrong.

Owning a home may seem way out of reach, but if you make a plan now and steadily work toward it, homeownership comes with serious long-term financial benefits.

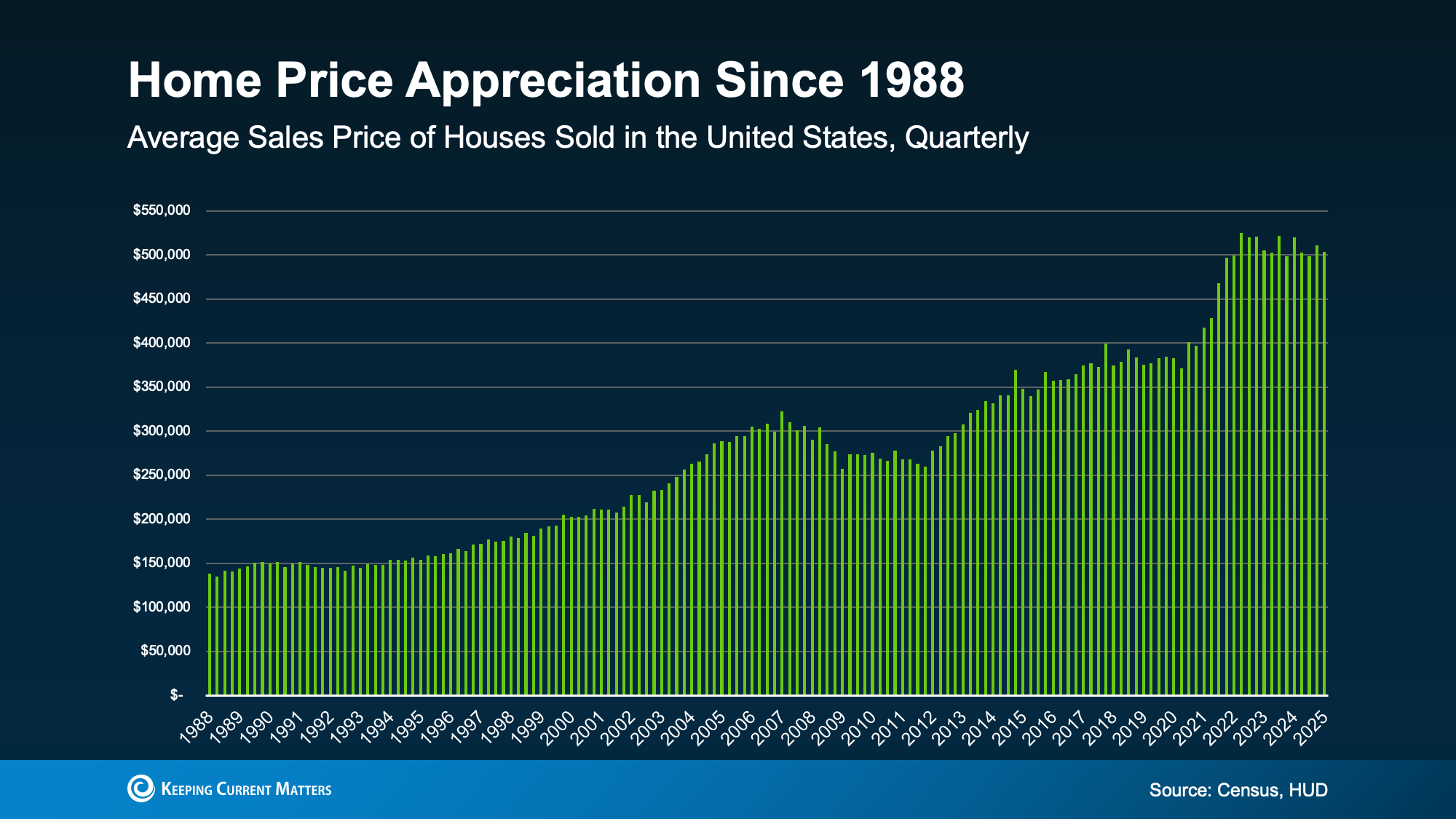

Homeownership Builds Wealth Over Time

Buying a home isn’t just about having a place to live – it’s a step toward building your future wealth.

Why? Home prices typically rise over time, which means the longer you wait, the more expensive it is to buy. And even in some markets where home prices are softening today, the overall long-term trend speaks for itself (see graph below):

And as home values rise, so does your equity when you’re a homeowner. That’s the difference between what your home is worth and what you owe. So, with every mortgage payment, that equity grows. Over time, that becomes part of your net worth.

And as home values rise, so does your equity when you’re a homeowner. That’s the difference between what your home is worth and what you owe. So, with every mortgage payment, that equity grows. Over time, that becomes part of your net worth.

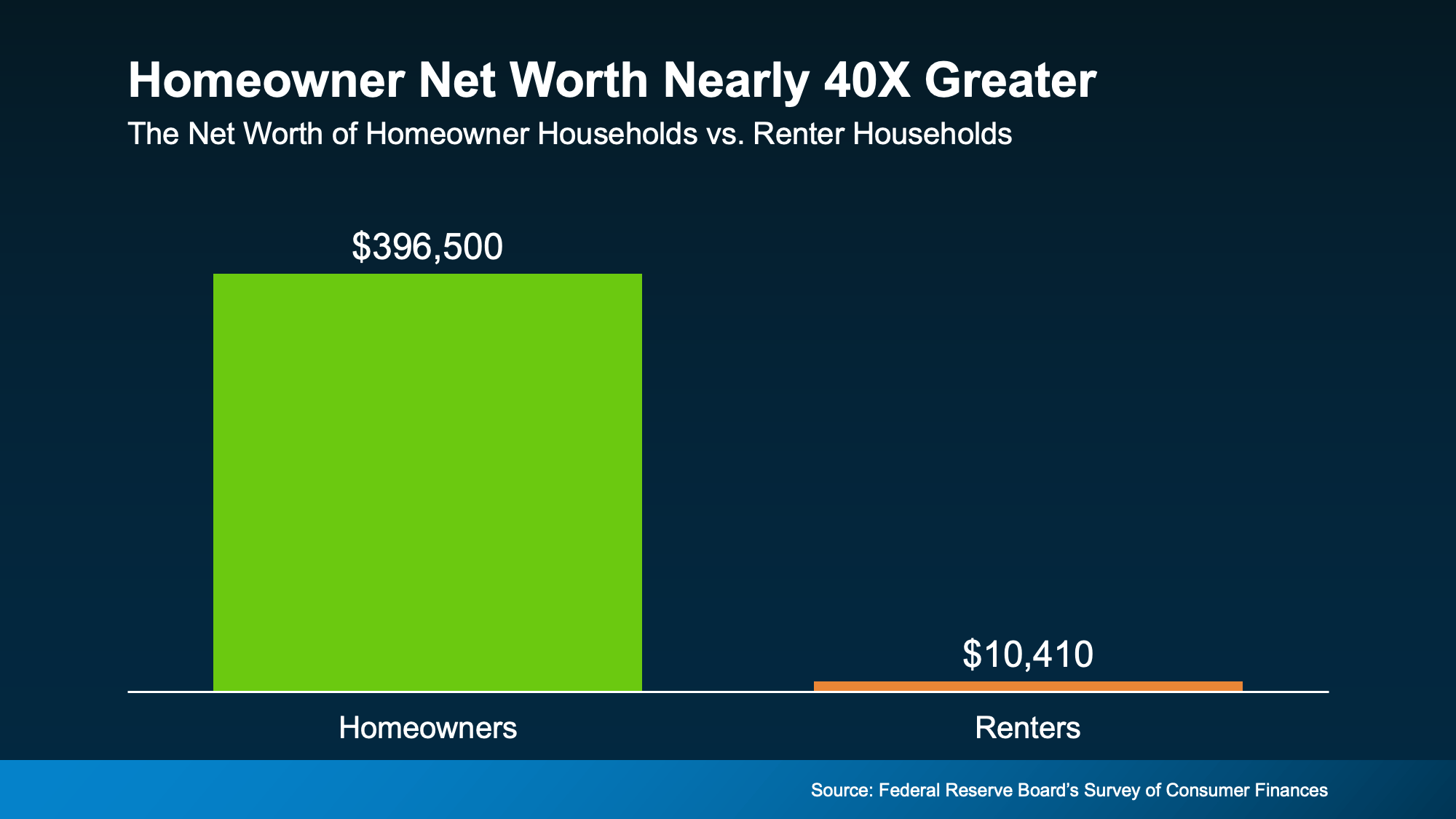

Today, the average homeowner’s net worth is nearly 40X greater than that of a renter. That’s a shocking difference, and the dollars in the visual below don’t lie (see graph below):

And it’s one of the big reasons why Forbes says:

And it’s one of the big reasons why Forbes says:

“While renting might seem like [the] less stressful option . . . owning a home is still a cornerstone of the American dream and a proven strategy for building long-term wealth.”

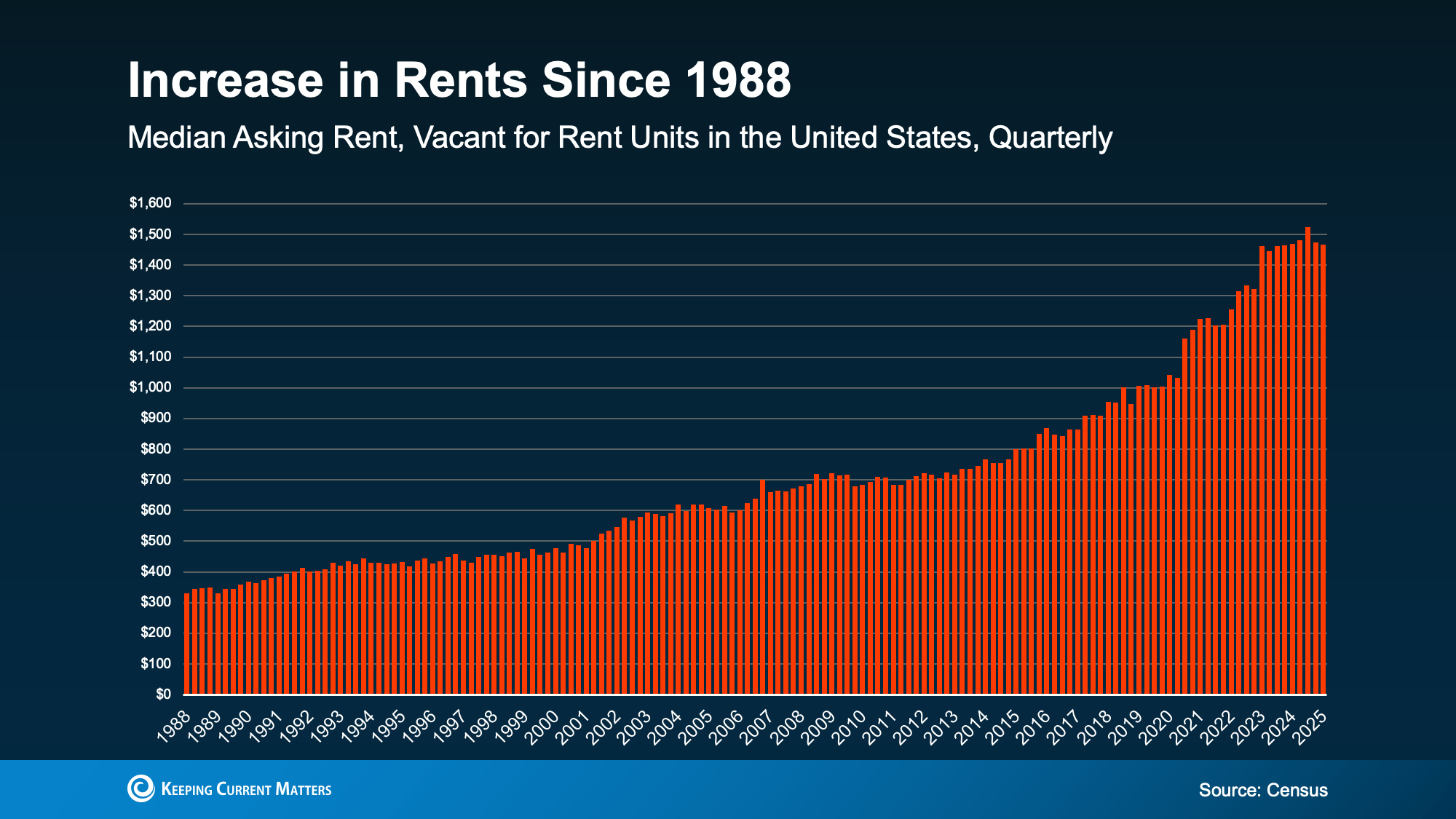

The Biggest Downside of Renting

So, short-term, why does renting feel like a simpler choice? Lower monthly payments, less responsibility, no strings attached. But long-term? It can sting.

For decades, while home prices have been rising, rent has gone up too. And while rent has held rather steady more recently, history shows the overall trend is up and to the right. That makes saving for a home more complicated than ever (see graph below):

That kind of financial uncertainty has a real impact. In the same Bank of America survey, 72% of potential buyers said they worry rising rent could affect their current and long-term finances.

That kind of financial uncertainty has a real impact. In the same Bank of America survey, 72% of potential buyers said they worry rising rent could affect their current and long-term finances.

Because rent doesn’t build wealth. It doesn’t come back to you later. It pays your landlord’s mortgage – not yours.

So, whether you rent or own, you’re paying a mortgage. The question is: whose mortgage do you want to pay?

Renting vs. Buying: What Really Matters

Think of it this way. Renting means your money is gone once you pay it. Owning means your payment builds equity – like a savings account you can live in. Sure, buying comes with responsibility. But it also comes with the kind of reward that grows over time. And that’s why you need a solid plan to get there.

As Joel Berner, Senior Economist at Realtor.com, explains:

“Households working on their budget will find it much easier to continue to rent than to go through the expenses of homeownership. However, they need to consider the equity and generational wealth they can build up by owning a home that they can’t by renting it. In the long run, buying a home may be a better investment even if the short-run costs seem prohibitive.”

Bottom Line

Renting may feel more do-able today. But over time, it could cost you more – without helping you build anything for your future.

If homeownership feels out of reach today, you’re not alone. And the first step toward getting out of the rental trap is to set a plan. Connect with an agent to set your specific goals and explore your options – so you’re ready when the time is right.

The Secret To Selling Your House in Today’s Market

A few years ago, homes were flying off the shelves and getting multiple offers well over their asking price. It felt like you could name your price and still have buyers lined up at the door.

But today’s housing market is different. Buyers are getting more selective now that inventory has grown. Homes are sitting a little longer. And more sellers are having to cut their prices.

So, how do you still come out on top? It all starts with one thing, pricing your house right from the start. Today, that matters more than ever – and it can make or break your sale.

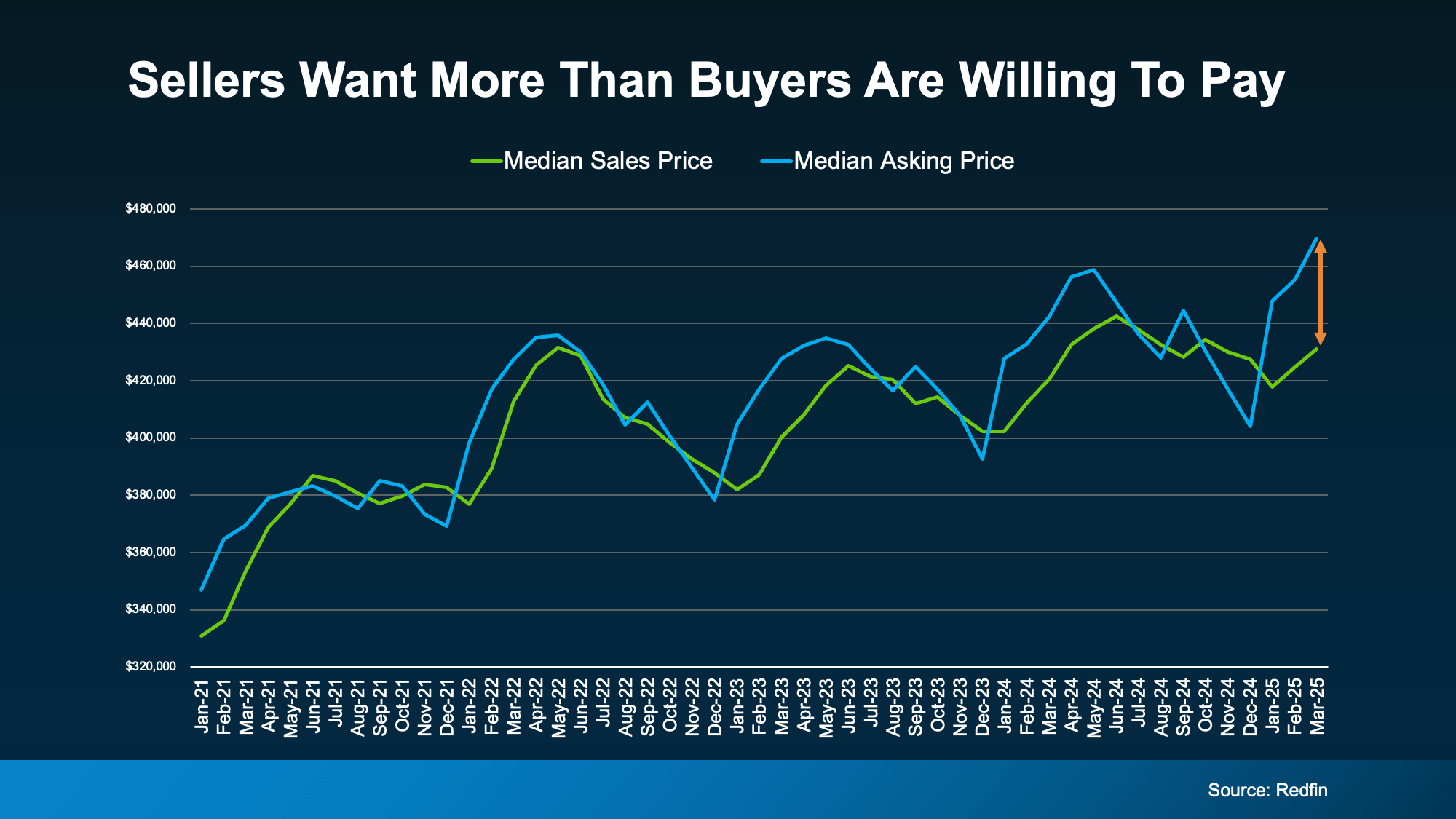

There’s a Real Price Disconnect Between Buyers and Sellers

A recent survey from Realtor.com shows 81% of home sellers believe they’ll get their asking price or more. But the actual sales data shows there’s a growing gap between what sellers expect and what buyers are actually willing to pay.

In fact, an annual report from the National Association of Realtors (NAR) shows 44% of recently sold homes went for less than the asking price. And 1 in 3 sellers had to cut their price at least once before the home sold. It’s a sign that expectations may be a little out of step with today’s reality.

Check out the graph below. It uses data from Redfin to show that asking prices (blue line) are higher than actual sales prices (green line) by a wider and wider margin:

This tells you something important: not all buyers are willing to pay what many sellers are asking. That doesn’t mean you can’t sell for a great price – but it does mean you need to start with a price that reflects what people are willing to pay in today’s market.

This tells you something important: not all buyers are willing to pay what many sellers are asking. That doesn’t mean you can’t sell for a great price – but it does mean you need to start with a price that reflects what people are willing to pay in today’s market.

What Happens When You Overprice Your House?

Pricing your house high initially may seem like a smart move, so you have more room to negotiate. But the reality is, an overpriced home can sit on the market and turn buyers away.

Buyers are smart. And when they see a house that’s been sitting for a while, they start to wonder what’s wrong with it. That can lead to fewer showings, less interest, and eventually, a price cut to re-ignite attention. As Realtor.com explains:

“By getting the right price early on, you can increase the odds buyers will be interested in the home. In turn, this decreases the chances the home will sit on the market for a lengthier timeline, also reducing the odds you’ll need to lower the listing price.”

The longer a house sits, the harder it can be to sell.

You Still Have a Great Opportunity – If You Price Your House Right

To avoid making this mistake, it’s important to lean on an agent who knows what’s happening locally when you set your asking price.

Your agent will look at recent local sales, buyer trends, and inventory levels to find that pricing sweet spot for your neighborhood – because it’s going to be different based on where you live.

And here’s something else to keep in mind, home prices have climbed more than 57% over the past five years. So, even if you price a bit below the number you had your sights set on, you’ll likely still be in a great position profit-wise.

With a local real estate agent’s help, you’ll attract more attention, avoid seeing your house sit on the market too long, and maximize your chances of getting a strong offer.

In today’s market, the right price works. As Mike Simonsen, Founder of Altos Research, explains:

“. . . the best properties, well priced are selling quickly in most of the country.”

Bottom Line

The market has changed, but your opportunity to sell hasn’t. You just need the right pricing plan. Talk to a local real estate agent to go over what’s happening with prices in your area and determine what price would help your house sell quickly and for top dollar.

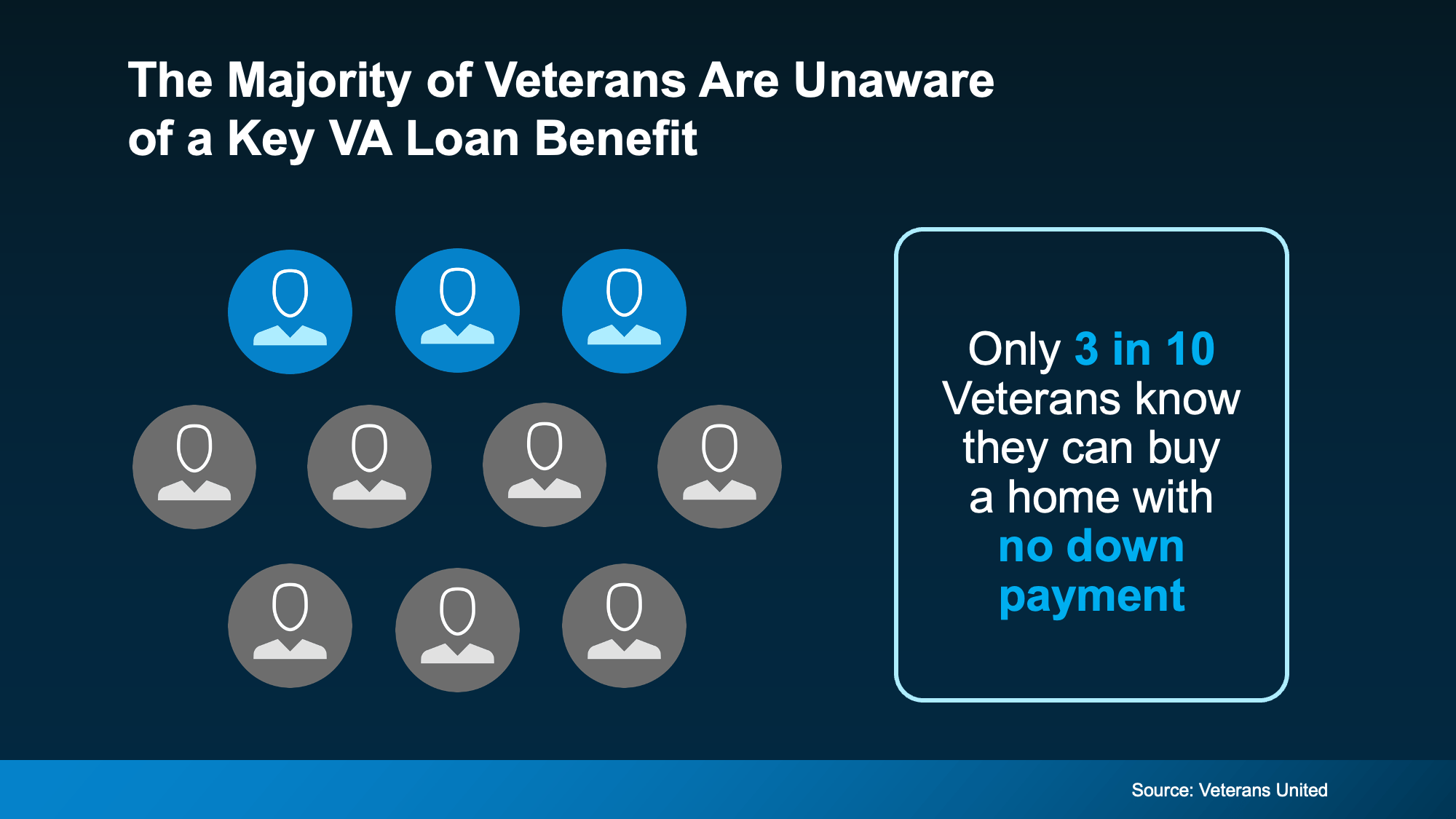

Many Veterans Don’t Know about This VA Home Loan Benefit

For 80 years, Veterans Affairs (VA) home loans have helped countless Veterans buy a home. But even though a lot of Veterans have access to this powerful program, the majority don’t know about one of its core benefits.

According to a report from Veterans United only 3 in 10 Veterans are aware they may be able to buy a home with no down payment with a VA loan (see visual below):

That means 7 out of every 10 Veterans could be missing out on a key homebuying advantage.

That means 7 out of every 10 Veterans could be missing out on a key homebuying advantage.

That’s why it’s so important for Veterans, and anyone who cares about a Veteran, to be aware of this program. As Veterans United explains, VA home loans:

“. . . come with a list of big-time benefits, including $0 down payment, no mortgage insurance, flexible and forgiving credit guidelines and the industry’s lowest average fixed interest rates.”

The Benefits of VA Home Loans

These loans are designed to make buying a home more achievable for those who have served. And, by extension, they also give their families the opportunity to plant roots and build equity in a home of their own. Here are some of the biggest advantages for this type of loan according to the Department of Veterans Affairs:

- Options for No Down Payment: One of the biggest perks is that many Veterans can buy a home with no down payment at all.

- Limited Closing Costs: With VA loans, there are limits on the types of closing costs Veterans have to pay. This helps keep more money in your pocket when you’re finalizing your purchase.

- No Private Mortgage Insurance (PMI): Unlike many other loan types, VA loans don’t require PMI, even with lower down payments. This means lower monthly payments, which can add up to big savings over time.

If you want to learn more, your best resource for all the options and advantages of VA loans is your team of expert real estate professionals, including a local agent and a trusted lender.

Bottom Line

VA home loans offer life-changing assistance, and a trusted lender and agent can help make sure you understand the details and are ready to move forward with a solid plan.

Do you know if you’re eligible for a VA home loan? Talk to a trusted lender who can help you see if you’d qualify.

Common Real Estate Terms Explained

If you’re a first-time homebuyer, chances are you’ll come across some terms you’re not familiar with. And that can be overwhelming, especially while going through one of the biggest purchases of your life.

The good news is you don’t need to be an expert on real estate jargon. That’s your agent’s job. But getting to know these basic terms will help you feel a lot more confident throughout the process.

Terms Every Homebuyer Should Know

Once you’re familiar with this terminology, you’ll have a better understanding of important details – from contracts to negotiations. So, when those big conversations happen, you’ll feel informed, in control, and able to make the best decision for your unique situation. As Redfin puts it:

“Having a basic understanding of important real estate concepts before you start the homebuying process will give you peace of mind now and could save you a fortune in the future.”

Here’s a breakdown of a few key real estate terms and definitions you should know, according to the Federal Trade Commission (FTC) and First American.

Appraisal: A report providing the estimated value of the home. Lenders rely on appraisals to determine a home’s value, so they’re not lending more than it’s worth.

Contingencies: Contract conditions that must be met, typically within a certain timeframe or by a specified date. For example, a home inspection is a common contingency. While you can waive these to try and make your offer more competitive, it’s generally not recommended.

Closing Costs: A collection of fees and payments made to the various parties involved in your home purchase. Ask your lender for a list of closing cost items, including attorney’s fees, taxes, title insurance, and more.

Down Payment: This varies by buyer, but is typically 3.5-20% of the purchase price of the home. There are even some 0% down programs available. Ask your lender for more information. Chances are, unless specified by your loan type of lender, you don’t need to put 20% down.

Escalation Clause: This is typically used in highly competitive markets. It’s an optional add on in a real estate contract that says a potential buyer is willing to raise their offer on a home if the seller receives a higher competing offer. The clause also includes how much a buyer is willing to pay over the highest offer.

Mortgage Rate: The interest rate you pay when you borrow money to buy a home. Consult a lender so you know how it can impact your monthly mortgage payment.

Pre-Approval Letter: A letter from a lender that shows what they’re willing to lend you for your home loan. This, plus an understanding of your savings, can help you decide on your target price range. Getting this from a lender should be one of your first steps in the homebuying process, before you even start browsing homes online.

Bottom Line

You don’t need to have all these terms memorized, but a little knowledge goes a long way. Brushing up on the basics now means fewer surprises later – and more clarity when you buy a home.

What unfamiliar real estate term or phrase have you come across that wasn’t on this list?

Connect with an agent to talk it through so you have a solid understanding of what it means and where it may show up in the homebuying process.

Real Estate Is Voted the Best Long-Term Investment 12 Years in a Row

Some Highlights

- In a recent poll from Gallup, real estate has once again been voted the best long-term investment. And it’s claimed that top spot for 12 straight years now.

- That’s because homeownership is one of the top ways to build your wealth, even with home price growth moderating and ongoing economic uncertainty.

- If you’ve been trying to decide if it makes sense to buy a home today, connect with an agent to talk about the programs that can help you become a homeowner.

Navigating Today’s Market

Wondering how to make sense of today’s housing market? You’re not alone. A lot of people are asking what’s ahead for inventory, prices, the economy, and more. You deserve answers — and that’s where your trusted local REMAX® agent comes in.

Weekend Projects To Boost the Value of Your Home

With the cost of just about everything going up these days — groceries, gas and utilities — you might be feeling like now just isn’t the time to take on any home projects. But remember, you don’t need to tackle a full-on renovation to make a big impact.

And if you don’t know where to start or what’s worth doing, lean on your trusted REMAX® agent for advice before you get your projects started.

Sometimes, small weekend projects still pack a big punch.

Here are a few examples of smart, budget-friendly updates you can do in just a few days to not only make your home feel fresh and new, but add value too.

One key place a lot of homeowners want to give some love? The kitchen. But instead of gutting the entire thing, think about smaller ways to give your space a facelift. You could go for new hardware, or maybe even add a backsplash. And if you want a refresh on your cabinets, consider bringing in a pro to paint or re-finish them. Just remember, the right tools are essential to a quality end product. Your REMAX agent can recommend local pros they trust, if you do need to hire someone to get the job done.

Another easy win? Light fixtures. This is one of the most overlooked updates, and one of the most affordable. Switch out that builder-grade fixture in your dining room or hallway for something a bit more modern or with a spark of personality. That’s an easy win to instantly change the feel of a room. And it doesn’t have to cost more than a nice dinner out.

Strategic bathroom refreshes are another great bang-for-your-buck project. You’ll be surprised the difference a new faucet, mirror or shower curtain can make. Add some fluffy towels and a plant or two, and suddenly you’ve got spa vibes on a shoestring budget.

Wallpaper is also having a moment right now — and is pretty affordable. Whether it’s the traditional variety or the peel-and-stick kind, a pattern can add interest and depth to a room. Just don’t overdo it. Sometimes too much can be overpowering.

And don’t underestimate the power of paint. A fresh, neutral coat on the walls can do wonders, especially if your current colors are looking a little tired or too specific. The right shade can brighten a room, make it feel bigger and create a clean, updated look.

The key is playing it smart with your budget.

None of these projects require a ton of time or a huge payout. You may not even need to hire a contractor. Focus on the little upgrades that make a big visual impact, because even in a time when everything feels more expensive, you still deserve to love your home.

This weekend, grab a coffee, throw on some music and knock out one small project. Your home (and future self) will thank you.

Bottom Line

When everything feels more expensive, it’s smart to focus on small updates that make a big impact. You don’t need a huge budget to love where you live. You just need a few good ideas (and maybe a little encouragement).

What’s on your weekend project list? If you’re ready to tackle those small-but-mighty upgrades, your trusted REMAX agent can help you prioritize what adds the most value. You don’t have to spend a fortune to make an impact.

What Buyers Need To Know About Homeowners Association Fees

When buying a home, you’re probably thinking about mortgage rates, home prices, your down payment, and maybe even your closing costs. But you may not be thinking about homeowners association (HOA) fees. While you won’t necessarily have these, you should know it’s a possibility, depending on where you decide to live.

A homeowners association is basically an organization that oversees a housing community (including shared spaces) and sets and enforces rules for things like upkeep. Some buyers love the perks that come with an HOA, others may see the fees as an extra expense. The key is knowing what they cover and whether the benefits outweigh the costs for you.

The Benefits of Having an HOA

Think about this. If you’ve fallen in love with a home because of how beautiful the community is – maybe it’s the landscaping, the well-maintained streets, or the overall curb appeal – there’s a good chance the HOA is one of the reasons why it looks so good. Here are some of the biggest perks:

- Neighborhood Maintenance: Many HOAs cover landscaping, snow removal, and upkeep of common areas. This helps maintain the neighborhood’s overall appearance.

- Amenities: Depending on the neighborhood, an HOA could also include access to perks like a pool, clubhouse, fitness center, or even private security. In these cases, while you have to pay an HOA fee, you’re also saving money in some ways because you don’t need to have separate gym or pool memberships anymore.

- Property Value Protection: Since HOAs enforce community standards, they prevent homes from falling into disrepair. So, you don’t have to worry about nearby eyesores hurting your property value.

- Less Personal Upkeep: In some communities, HOAs even take care of exterior maintenance, roof repairs, or other shared responsibilities, reducing the work for homeowners.

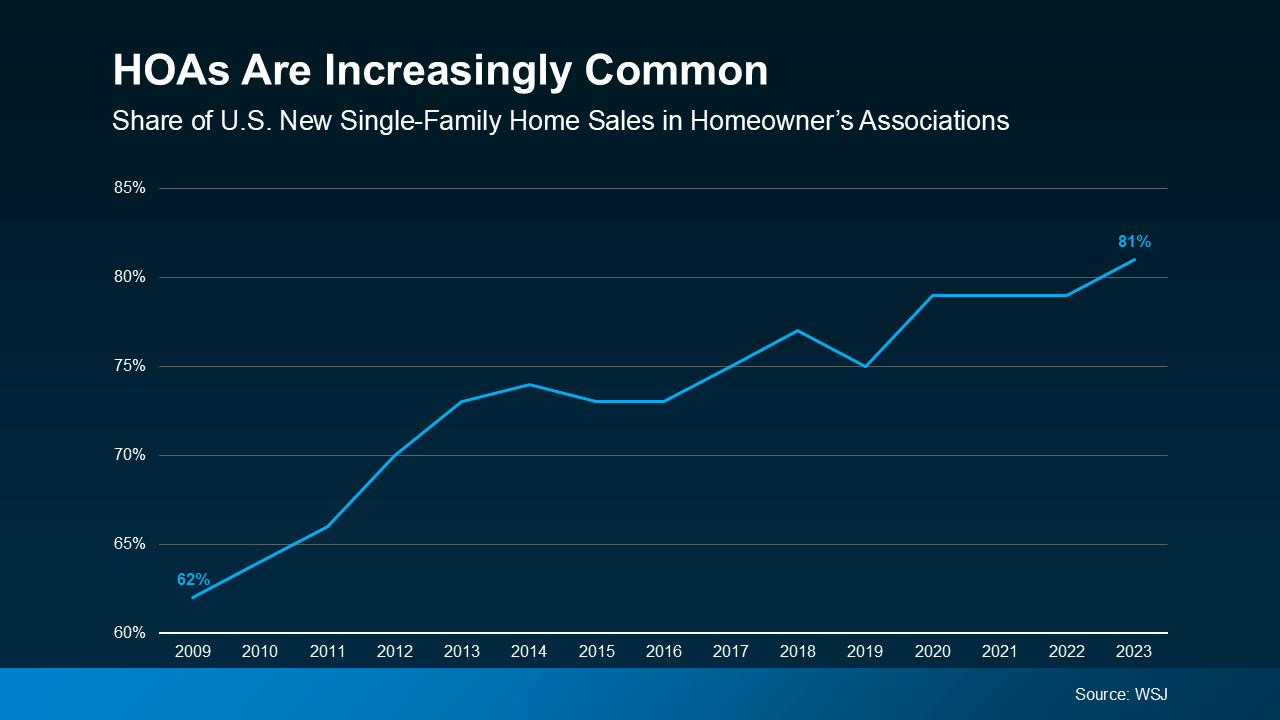

HOA Fees: More Common, Especially in Newer Neighborhoods

Does every house have HOA fees? No, not all homes have them. But they are common, especially in newer communities. In fact, over 80% of newly built single-family homes are now part of an HOA, according to the Wall Street Journal (see graph below):

But it’s not just new builds that have homeowners associations. Homes that were previously lived in may have an HOA fee too. According to Axios roughly 4 out of every 10 homes had an HOA in 2024.

But it’s not just new builds that have homeowners associations. Homes that were previously lived in may have an HOA fee too. According to Axios roughly 4 out of every 10 homes had an HOA in 2024.

HOA Fees and Your Home Search

Ask your agent about which homes do and do not have HOA fees as part of your search – and how much the fees are. Some neighborhoods have quarterly dues, some have monthly, some don’t have any at all. To give you some sort of baseline though, the median HOA fee rose last year to $125 per month, based on a report from Realtor.com.

But remember, the costs vary and sometimes these fees give you access to great perks. As Danielle Hale, Chief Economist at Realtor.com, explains:

“When considering a home with an HOA, buyers should work to understand what benefits it provides like maintenance, security, or communal amenities, and how the HOA fees factor into their overall budget.”

Bottom Line

Before buying a home in an HOA community, it’s a good idea to review the rules and fees so you know exactly what’s included, how that fits into your overall budget, and what restrictions may apply.

Would you rather pay an HOA fee for added perks, or skip it and have full control over your property? Connect with an agent to talk about what’s best for you.

You Could Use Some of Your Equity To Give Your Children the Gift of Home

If you’re a homeowner, chances are you’ve built up a lot of wealth – just by living in your house and watching its value grow over time. And that equity? It’s something that could help change your child’s life.

Since affordability is still a challenge, a lot of first-time buyers are struggling to buy a home in today’s market. Even if they have a stable job and a solid plan, buying can still feel out of reach. But that’s where your equity could make all the difference.

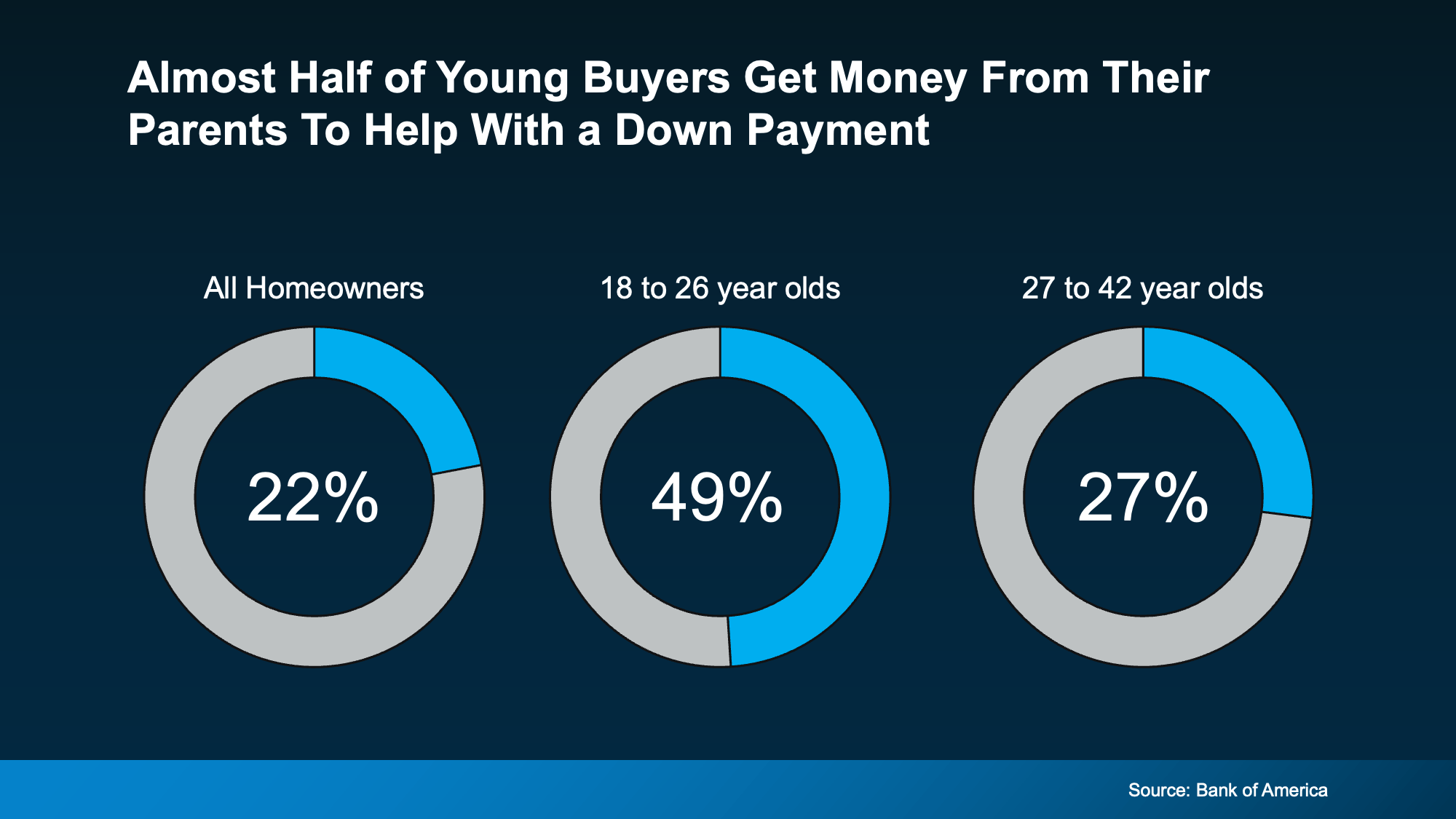

To give you an idea, the average homeowner with a mortgage has $311,000 worth of equity, according to Cotality (formerly CoreLogic). That’s significant. And some parents are using a portion of their equity to help their children become homeowners, too.

According to Bank of America, 49% of buyers between 18 and 26 got money from their parents to use toward their down payment (see chart below):

Even though the data doesn’t specify how many parents used their equity, the wealth they’ve built through homeownership may have helped make it possible – especially given how much equity the average homeowner has today.

Even though the data doesn’t specify how many parents used their equity, the wealth they’ve built through homeownership may have helped make it possible – especially given how much equity the average homeowner has today.

While what’s right for each person’s specific situation will vary on a case-by-case basis, that’s a powerful legacy to pass on. It helps those younger people buy a home, build equity of their own, and begin the next chapter of their life with a little less financial stress and a lot more stability. And for those parents? It’s a way to turn what they’ve built into something deeply meaningful.

This isn’t just about money. For many homeowners, it’s about being the reason their child gets to say, “we got the house.” And giving them the kind of head start they might’ve only dreamed of at their age. And here’s the part that really sticks. Compare the Market says:

“Of those who did receive monetary aid from parents and grandparents to buy a house, 45% of Americans said they would not have been able to purchase a house without financial support from parents and grandparents.”

Bottom Line

Your equity could be the thing that makes homeownership possible for your children when they might not be able to do it on their own. So, here’s the question.

If helping your kids buy a home was more feasible than you thought, would you want to explore that option?

If you want to learn more or find out the best way to make it happen, talk to your lender and a financial advisor you trust.