Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Congratulations to the 2026 recipients of the ERA Central EDGE Scholarship!

Through their applications, these young people have shown that they embody the same ideals for which our Realtor® professionals are so well known: Ethics, Dedication, Genuineness and an Entrepreneurial spirit.

The scholarship program, which began in 2005, is funded by the Realtor of ERA Central Realty Group and matched by the company. It was founded based on giving back to the community and honoring the families that have supported ERA Central for more than three decades. Since its inception, the EDGE Scholarship has awarded $90,000 in scholarships.

Through their inspiring applications, these exceptional young people have proven that they share the very same values our ERA Central Realtors® are known for: unwavering ethics, genuine dedication, and an entrepreneurial drive to make a difference.

Established in 2005, the EDGE Scholarship program is a true testament to our belief in giving back. Funded by the committed Realtors® of ERA Central Realty Group and matched by the company, this program honors the families who have supported us for more than thirty years. Since its beginning, the EDGE Scholarship has proudly awarded over $85,000 to deserving local students.

|

Varnika Neeli Freehold Township |

Nicolas Chavez Northern Burlington |

Sanat Golecha West Windsor |

Brendan Melchior New Egypt |

|

|

|

|

Philip Angarone, Realtor® and Scholarship Committee Chairperson says of this year’s competition, “All of the 60 applicants from 24 central New Jersey high schools provided impressive applications. Our winners should be very proud of themselves!”

To learn more about the scholarship and to apply, visit EDGEscholarship.com

![]()

8th Annual Shred Event April 25th 2026!

FREE SHREDDING EVENT!

CREAM RIDGE SATURDAY, APRIL 25th, 2026 10am to 1pm 210 Route 539, Cream Ridge

Spring Cleaning? Bring your documents to the FREE SHREDDING EVENT at our Cream Ridge office (210 Route 539) on Saturday, April 25th from 10 am to 1 pm just pop the trunk and we’ll do the rest! No need to remove paper clips, staples, hanging file folders, etc. ITEMS NOT ACCEPTED:

3-Ring Binders

Media Items

Metal Objects

Computer Hard Drives

CDs and Cases

Plastic Objects

X-Rays

In the event that the line is long, you will be permitted five boxes at a time. You are welcome to get in the line as many times as you wish, as long as time and shred space allows.

Identity theft remains a growing threat to American consumers. In 2024, 2.6 million U.S. consumers lost more than $12.5 billion to fraud – a 25% jump over 2023, according to the Federal Trade Commission. This included 1.1 million reports of identity theft – up 18% over 2023. Hijacked and newly opened bogus credit cards are the most common form of identity theft, according to Experian. Shred-it is an information security solution provided by Stericycle, Inc. From medical waste and document destruction to compliance solutions, our entire team has been protecting what matters since 1989.

This free event is sponsored by ERA Central Realty Group as part of its ongoing community outreach mission. ERA Central Realty has been a part of the Plumsted, Cream Ridge, and Allentown community for over 40 years. ERA Central and its agents are involved in many charitable and community efforts, such as MDA Summer Camp, Project One, Move for Hunger, and their own EDGE Scholarship, for which over $80,000 has been awarded to local college-bound high school students since 2005.

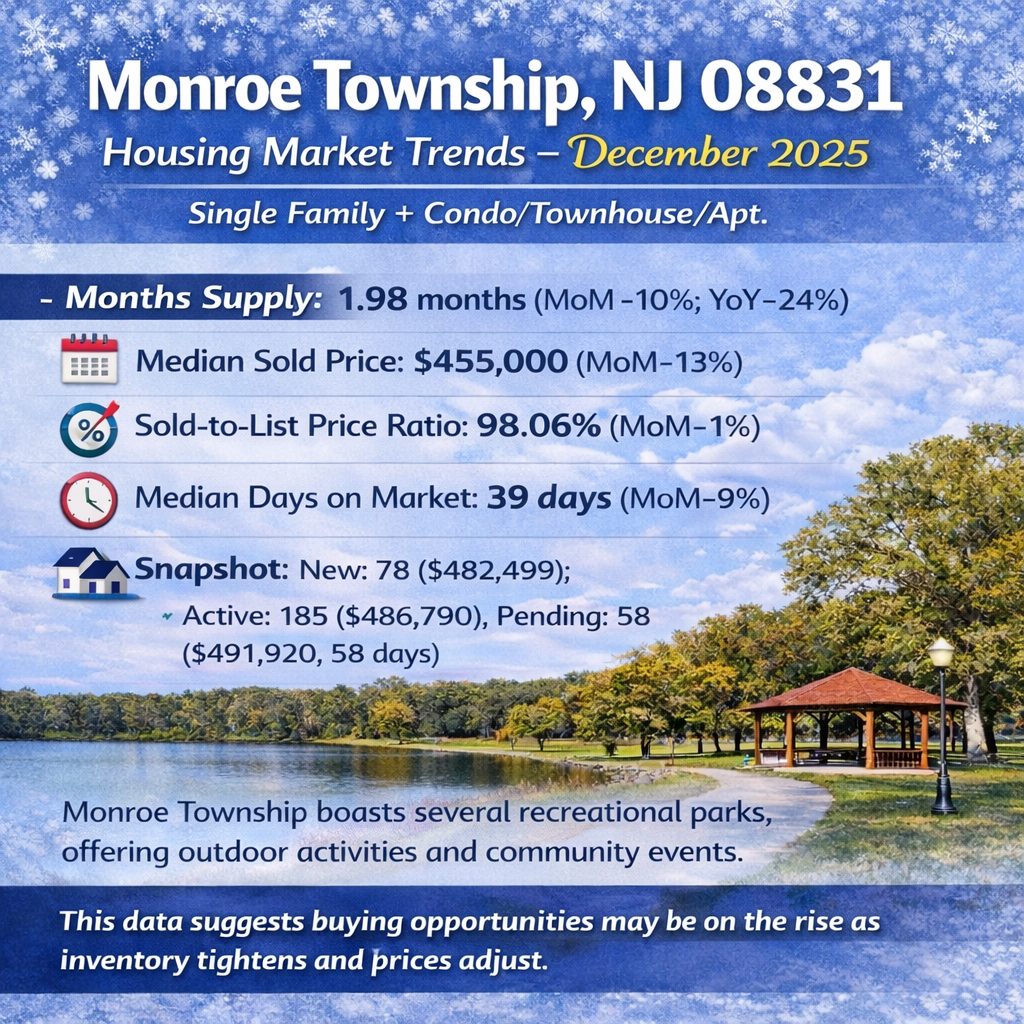

Monroe Township, NJ 08831 Market Trends: December 2025

Monroe Township, NJ 08831, December 2025, Single Family + Condo/Townhouse/Apt.

Are prices rising?

The median sold price for homes in Monroe Township is $455,000, reflecting a 13% decrease month-over-month, indicating some price softening in the market.

How’s the inventory?

Inventory levels show a months supply of 1.98, with a 10% decrease from the previous month and a 24% decrease over the past year, suggesting a tighter market for buyers.

What’s the trend with listings?

There are 78 new listings with a median list price of $482,499, while active listings hold a median price of $486,790, offering a range of options for prospective buyers.

How quickly are homes selling?

Homes are moving quickly with new pending listings having a median of 58 days in RPR and a median sold price maintaining a strong 98.06% of the list price, despite a slight 1% month-over-month decrease.

Monroe Township offers enriching community attractions like Thompson Park and convenient access to major highways, enhancing its appeal. For personalized insights and to navigate your home buying journey in Monroe Township, connect with one of our ERA Central Realty Group agents.

Roslyn Sibilia Earns Broker★Agent Advisor “Seven Star – Top 100 Referral Partner” for New Jersey — Again in 2025

Cream Ridge, NJ — October 2025 — ERA Central Realty Group is proud to share that Roslyn Sibilia has once again been recognized by Broker★Agent Advisor as a “Seven Star – Top 100 Referral Partner” honoree for the state of New Jersey. This marks Roslyn’s second consecutive year receiving this outstanding honor, celebrating her unwavering commitment to client care, market expertise, and results.

“Roslyn’s repeat recognition says it all,” said Scott Lauri, CEO of ERA Central Realty Group. “Her follow-through, professionalism, and heart for service set a standard our whole company strives to meet.”

“I’m truly grateful,” said Roslyn Sibilia. “Being named again in 2025 reflects the trust my clients place in me and the support of my ERA Central family. I’m committed to guiding every buyer and seller with clarity, care, and confidence.”

Why this recognition matters

-

Top-tier service: The Seven Star distinction highlights consistent, high-quality client experiences.

-

Strong referral network: “Top 100 Referral Partner” status underscores Roslyn’s reputation among peers—agents trust sending their clients to her.

-

Local market impact: Roslyn’s guidance helps NJ buyers and sellers make smart moves, from pricing to negotiation to closing.

Whether you’re planning to buy, sell, or simply want a clear read on today’s market, connect with Roslyn Sibilia at 732-995-5609.

About ERA Central Realty Group

ERA Central Realty Group serves communities across Central New Jersey with a culture of service, education, and results-driven representation for buyers, sellers, and investors.

2025 Shred Event in Bordentown

FREE SHREDDING EVENT!

BORDENTOWN

SATURDAY, SEPTEMBER 20th 2025

9am to 12pm

3379 US 206, Bordentown, NJ 08505

Open to our neighbors in Bordentown, Mansfield, and Chesterfield and past clients of ERA Central Realty Group

Bring your documents to the FREE SHREDDING EVENT at our Bordentown office (3379 US 206) on Saturday, June 3rd from 9am to 12pm. This contactless event is open to our neighbors in Bordentown, Mansfield, and Chesterfield – just pop the trunk and we’ll do the rest!

No need to remove paper clips, staples, hanging file folders, etc.

ITEMS NOT ACCEPTED:

- 3-Ring Binders

- Media Items

- Metal Objects

- Computer Hard Drives

- CDs and Cases

- Plastic Objects

- X-Rays

In the event that the line is long, you will be permitted five boxes at a time. You are welcome to get in the line as many times as you wish, as long as time and shred space allows.

Identity theft is one of the fastest growing non-violent crimes in America. It impacts nearly 9 million victims each year, and approximately 75% of cases are a result of paper documents getting into the wrong hands. Proper destruction of confidential documents is a critical step in ensuring members of the community do not become victims of identity theft.

A community-wide shred event sponsored by ERA Central Realty Group makes it possible for members of the community to reduce their exposure to identity theft risk by having their personal and confidential materials securely destroyed in a Shred-It state-of-the-art mobile shredding truck.

THE SHRED-IT DIFFERENCE

We Protect What Matters.

Shred-it delivers more than just secure shredding—we provide peace of mind. Our fully customizable solutions are designed to fit your unique business needs, and our dedicated team is always ready to support you with flexible, convenient service. We protect what matters, offering industry-leading expertise, top-level security, and environmentally responsible practices.

This free event is sponsored by ERA Central Realty Group as part of its ongoing community outreach mission. ERA Central Realty has been a part of the Bordentown, Mansfield, and Chesterfield community for over 40 years. ERA Central and its agents are involved in many charitable and community efforts, such as MDA Summer Camp, Project One, Move for Hunger, and their own EDGE Scholarship, for which over $90,000 has been awarded to local college-bound high school students since 2005.

Congratulations to the 2025 recipients of the ERA Central EDGE Scholarship!

Through their applications, these young people have shown that they embody the same ideals for which our Realtor® professionals are so well known: Ethics, Dedication, Genuineness and an Entrepreneurial spirit.

The scholarship program, which began in 2005, is funded by the Realtor of ERA Central Realty Group and matched by the company. It was founded based on giving back to the community and honoring the families that have supported ERA Central for more than three decades. Since its inception, the EDGE Scholarship has awarded $85,000 in scholarships.

Through their inspiring applications, these exceptional young people have proven that they share the very same values our ERA Central Realtors® are known for: unwavering ethics, genuine dedication, and an entrepreneurial drive to make a difference.

Established in 2005, the EDGE Scholarship program is a true testament to our belief in giving back. Funded by the committed Realtors® of ERA Central Realty Group and matched by the company, this program honors the families who have supported us for more than thirty years. Since its beginning, the EDGE Scholarship has proudly awarded over $85,000 to deserving local students.

|

Lindsey Reed |

Emily Laing |

Nicholas Yagnik |

Madeline Ruchelman |

|

|

|

|

Philip Angarone, Realtor Associate® and Scholarship Committee Chairperson says of this year’s competition, “All of the 79 applicants from 34 central New Jersey high schools provided impressive applications. Our winners should be very proud of themselves!”

To learn more about the scholarship and to apply, visit EDGEscholarship.com

![]()

The Rooms That Matter Most When You Sell

Now that buyers have more options for their move, you need to be a bit more intentional about making sure your house looks its best when you sell. And proper staging can be a great way to do just that.

What Is Home Staging?

It’s not about making your house look super trendy or like it belongs in a magazine. It’s about helping it feel welcoming and move-in ready, so it’s easy for buyers to picture themselves living there.

It’s important to understand there’s a range when it comes to staging. It can include everything from simple tweaks to more extensive setups, depending on your needs and budget. But a little bit of time, effort, and money invested in this process can really make a difference when you sell – especially in today’s market.

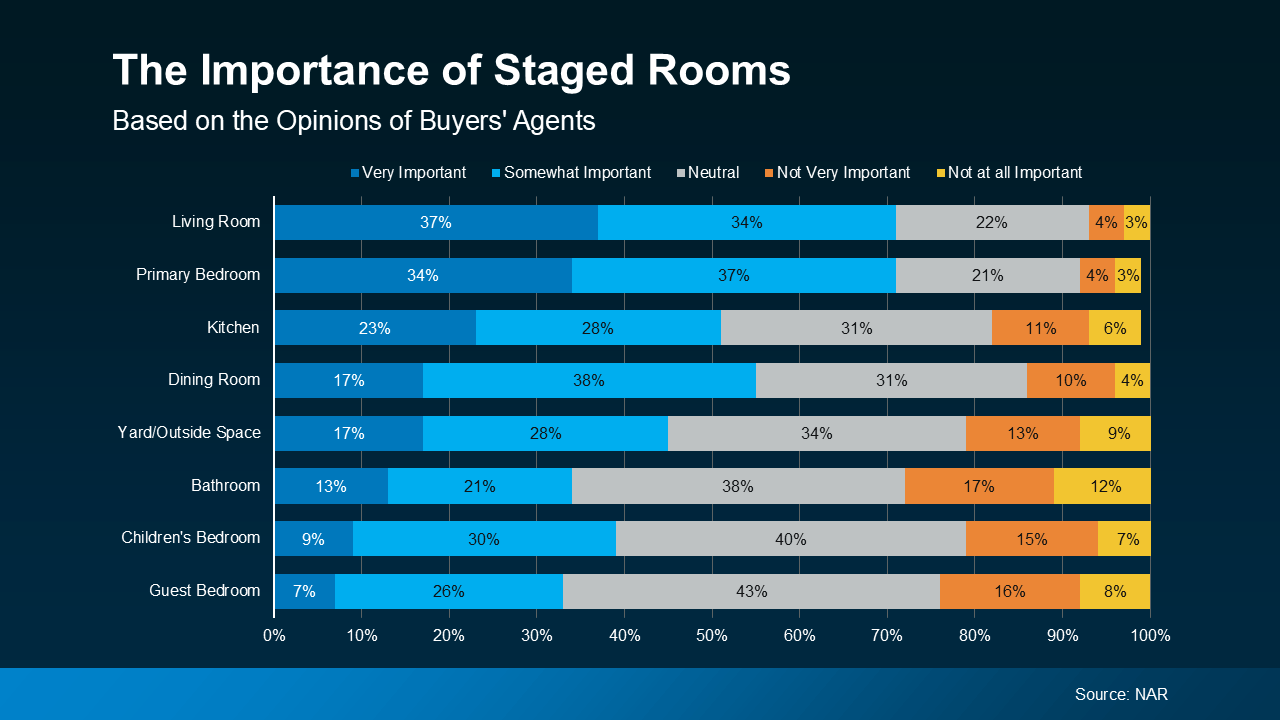

A study from the National Association of Realtors (NAR) shows staged homes sell faster and for more money than homes that aren’t staged at all (see below):

Which Rooms Matter Most?

The best part is, odds are you don’t have to stage your whole house to make an impact. According to NAR, here’s where buyers’ agents say staging can make the biggest difference (see graph below):

As you can see, agents who talk to buyers regularly agree, the most important spaces to stage are the rooms where buyers will spend the most time, like the living room, primary bedroom, and kitchen.

As you can see, agents who talk to buyers regularly agree, the most important spaces to stage are the rooms where buyers will spend the most time, like the living room, primary bedroom, and kitchen.

While this can give you a good general idea of what may be worth it and what’s probably not, it can’t match a local agent’s expertise.

How an Agent Helps You Decide What You Need To Do

Agents are experts on what buyers are looking for where you live, because they hear that feedback all the time in showings, home tours, walkthroughs, and from other agents. And they’ll use those insights to give their opinion on your specific house and what areas may need a little bit of staging help, like if you need to:

- Declutter and depersonalize by removing photos and personal items

- Arrange your furniture to improve the room’s flow and make it feel bigger

- Add plants, move art, or re-arrange other accessories

A lot of buyers can use the agent’s know-how as the only staging advice they need. But, if your home needs more of a transformation, or it’s empty and could benefit from rented furniture, a great agent will be able to determine if bringing in a professional stager might be a good idea, too. Just know that level of help comes with a higher price tag. NAR reports:

“The median dollar value spent when using a staging service was $1,500, compared to $500 when the sellers’ agent personally staged the home.”

A local agent will help you weigh the costs and benefits based on your budget, your timeline, and the overall condition of your house. They’ll also consider how quickly similar homes are selling nearby and what buyers are expecting at your price point.

Bottom Line

Staging doesn’t have to be over-the-top or expensive. It just needs to help buyers feel at home. And a great agent will help you figure out the level of staging that makes the most sense for your goals.

Which room in your house do you think would make the biggest impression on a buyer?

Get an agent to walk through your home with you and go over what will make your house stand out.

Understanding Today’s Mortgage Rates: Is 3% Coming Back?

A lot of buyers are pressing pause on their plans these days, holding out hope that mortgage rates will come down – maybe even back to the historic-low 3% from a few years ago. But here’s the thing: those rates were never meant to last. They were a short-term response to a very specific moment in time. And as the market finds its footing again, it’s time to reset expectations.

Back in 2020 and 2021, 3% mortgage rates gave buyers a serious boost: more affordability, more buying power, and more opportunity. But those rates were a result of emergency economic policies during the height of a global pandemic. Now that the economy is in a different place, we’re seeing mortgage rates in the high 6% to low 7% range.

And while experts currently project a slight easing in the months ahead, most industry leaders agree: rates are not going back to 3%.

Instead, many forecasts suggest mortgage rates will settle in the mid-6% range by the end of the year, pending any major economic shifts. As Kara Ng, Senior Economist at Zillow, says:

“While Zillow expects mortgage rates to end the year near mid-6%, barring any unforeseen shocks, that path might be bumpy.”

What Buyers Should Know

Basically, waiting for 3% rates might mean waiting longer than you’d expect – and missing out along the way. Instead of putting off homebuying indefinitely, make a plan to get there and focus on what you can control: your budget, your credit, and working with a trusted professional who can explain exactly what’s happening in the current market – and how to navigate it.

Your local real estate agent and a trusted lender make all the difference in this process. The experts have insights into down payment assistance programs, alternative financing options, negotiation strategies, and overall – the experience you need on your side to understand creative ways that will make your plans work.

And here’s the biggest thing to keep in mind. Since rates are projected to ease slightly later this year, if that happens, it could bring some more buyers back into the market. Acting now gives you a head start, especially with more homes on the market than we’ve seen in years.

Think about it: if mortgage rates do come down, what do you think everyone else is going to do? That’s right – they’ll jump back in too.

Getting ahead of that rush could put you in a stronger position to find the right home with less competition. Realtor.com sums it up well:

“Staying out of the market in hopes of a rate drop that never comes can lead to missed opportunities . . . Rising home prices, rent increases, and inflation might outpace any future savings on interest. And if rates do fall sharply again, buyers could face an entirely different challenge: surging competition.”

Bottom Line

Those 3% rates everyone remembers from a few years ago were the exception, not the rule.

Now that they’re settling into new territory, it’s a good time to adjust your expectations and learn more about where things are heading as this market shifts.

A local real estate agent and a trusted lender will be your best resources, always keeping you up-to-date and informed, so you can make sense of your options and build a game plan that works for you.

Why Buying Real Estate Is Still the Best Long-Term Investment

Lately, it feels like every headline about the housing market comes with a side of doubt. Are prices going up or down? Are we headed for a crash? Will rates ever come down? And all the media noise may leave you wondering: does it really make sense to buy a home right now?

But here’s one thing that doesn’t get enough airtime. Real estate has always been about the long game. And when you look at the big picture, not just the latest clickbait headlines, it’s easy to see why so many people say it’s still the best investment you can make – even now.

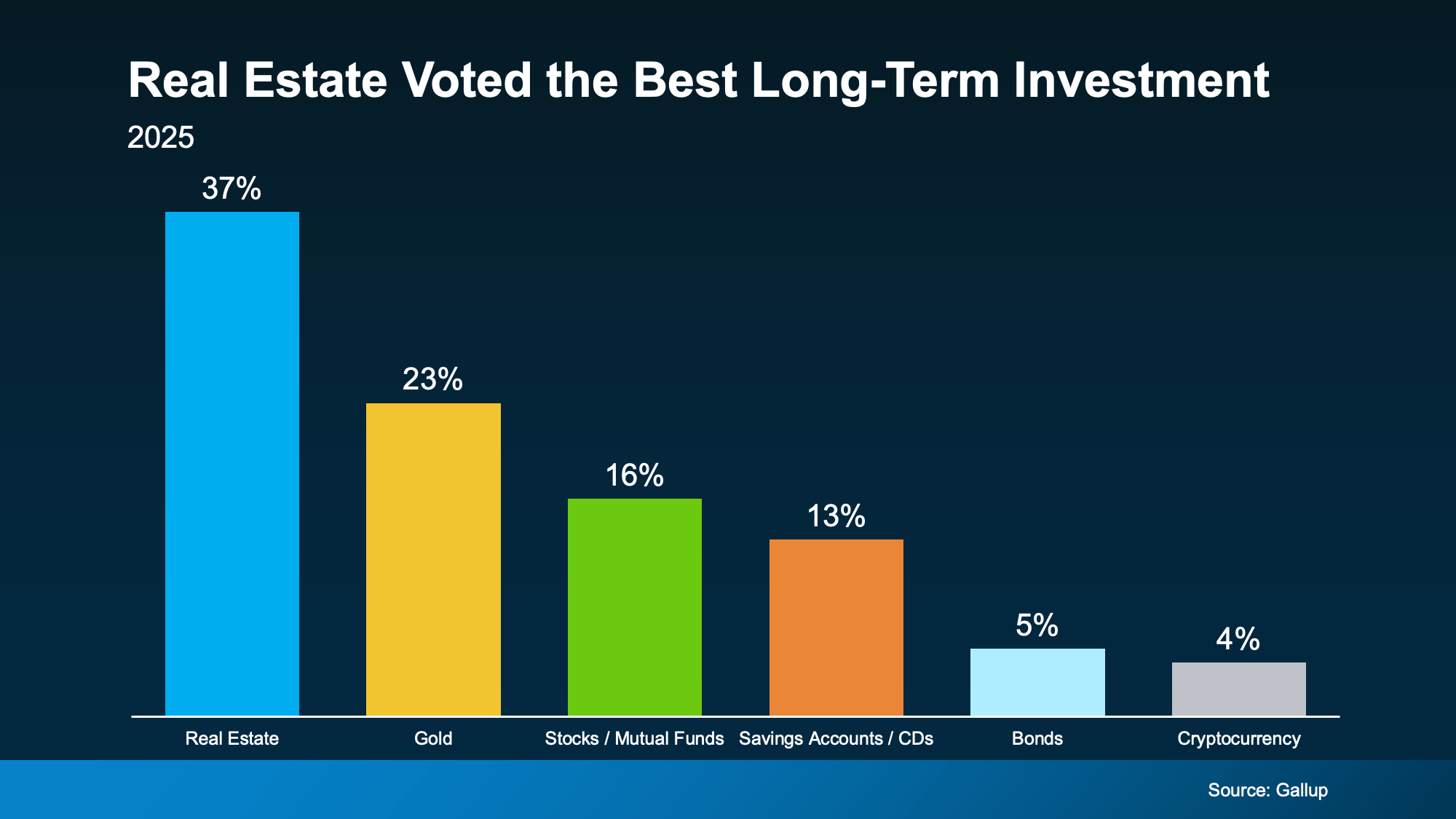

According to the just-released annual report from Gallup, real estate has been voted the best long-term investment for the 12th year in a row. That’s over a decade of beating out stocks, gold, and bonds as America’s top pick.

And this isn’t new. Real estate usually claims the #1 title. But here’s what’s really interesting. This year’s results came in just after a rocky April for the stock and bond markets. It shows that, even as other investments had wild swings, real estate has held its ground. That’s likely because it gains value in a steadier, more predictable way. As Gallup explains:

And this isn’t new. Real estate usually claims the #1 title. But here’s what’s really interesting. This year’s results came in just after a rocky April for the stock and bond markets. It shows that, even as other investments had wild swings, real estate has held its ground. That’s likely because it gains value in a steadier, more predictable way. As Gallup explains:

“Amid volatility in the stock and bond markets in April, Americans’ preference for stocks as the best long-term investment has declined. Gold has gained in appeal, while real estate remains the top choice for the 12th consecutive year.”

That says a lot. Even though things may feel a bit uncertain in today’s economy, real estate can still be a powerful investment.

Yes, home values are rising at a more moderate pace right now. And sure, in some markets, prices may be flat in the year ahead or even dip a little – but that’s just the short-term view. Don’t let that cloud the bigger picture.

Real estate has a long track record of gaining value over time. That’s the kind of growth you can count on, especially if you plan to live in that home for a long time.

That’s part of why Americans continue to buy-in to homeownership – even when the headlines may sound a little uncertain. As Sam Williamson, Senior Economist at First American, says:

“A home is more than just a place to live—it’s often a family’s most valuable financial asset and a cornerstone to building long-term wealth.”

Bottom Line

Real estate isn’t about overnight wins. It’s about long-term gains. So, don’t let the uncertainty in a shifting market make you think it’s a bad time to buy.

If you’re feeling unsure, just remember: Americans have consistently said real estate is the best long-term investment you can make. And if you want more information about why so many people think homeownership is worth it, reach out to a local real estate agent.

Newly Built Homes May Be Less Expensive Than You Think

Do you think a brand-new home means a bigger price tag? Think again.

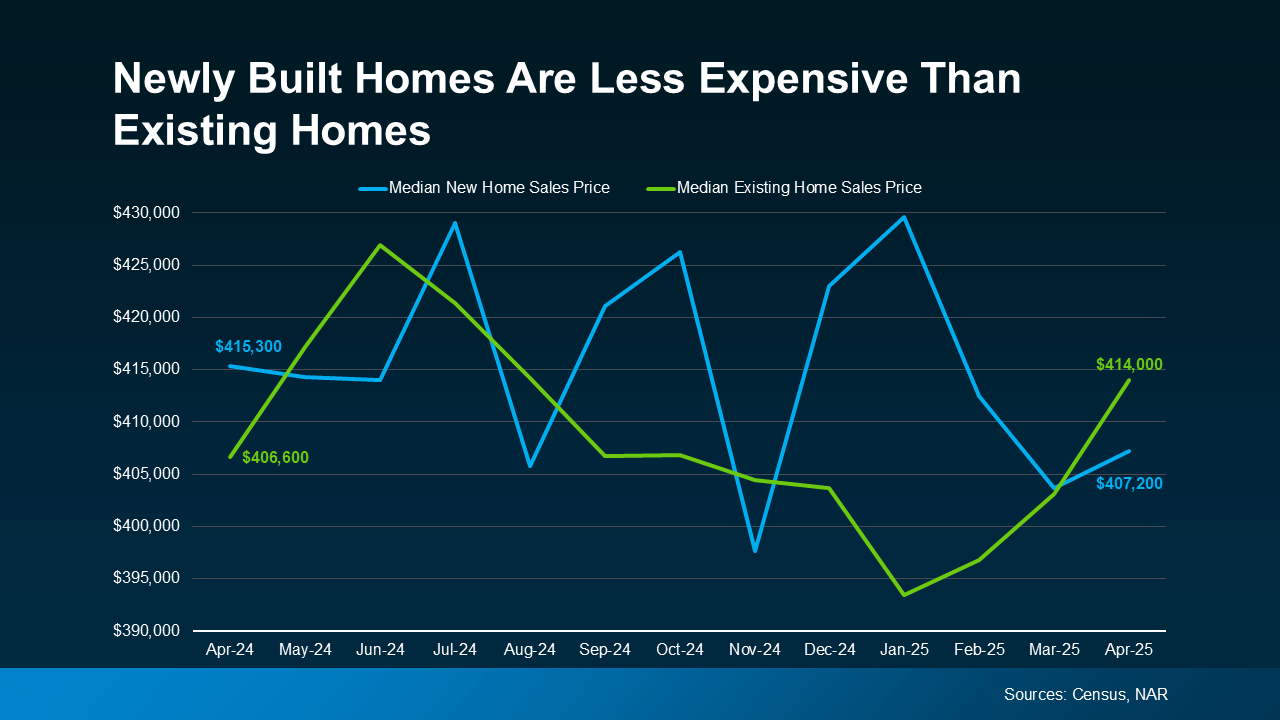

Right now, something unique is happening in the housing market. According to the Census and the National Association of Realtors (NAR), the median price of newly built homes is actually lower than the median price for existing homes (ones that have already been lived in):

You read that right. That brand new, never-been-lived-in house may cost less than the one built 20 years ago in a neighborhood just down the street. So, if you wrote off a new build because you assumed they’d be financially out of reach, here’s what you should know. You could be missing out on some of the best options in today’s housing market.

You read that right. That brand new, never-been-lived-in house may cost less than the one built 20 years ago in a neighborhood just down the street. So, if you wrote off a new build because you assumed they’d be financially out of reach, here’s what you should know. You could be missing out on some of the best options in today’s housing market.

Why Are Newly Built Homes Less Expensive Right Now?

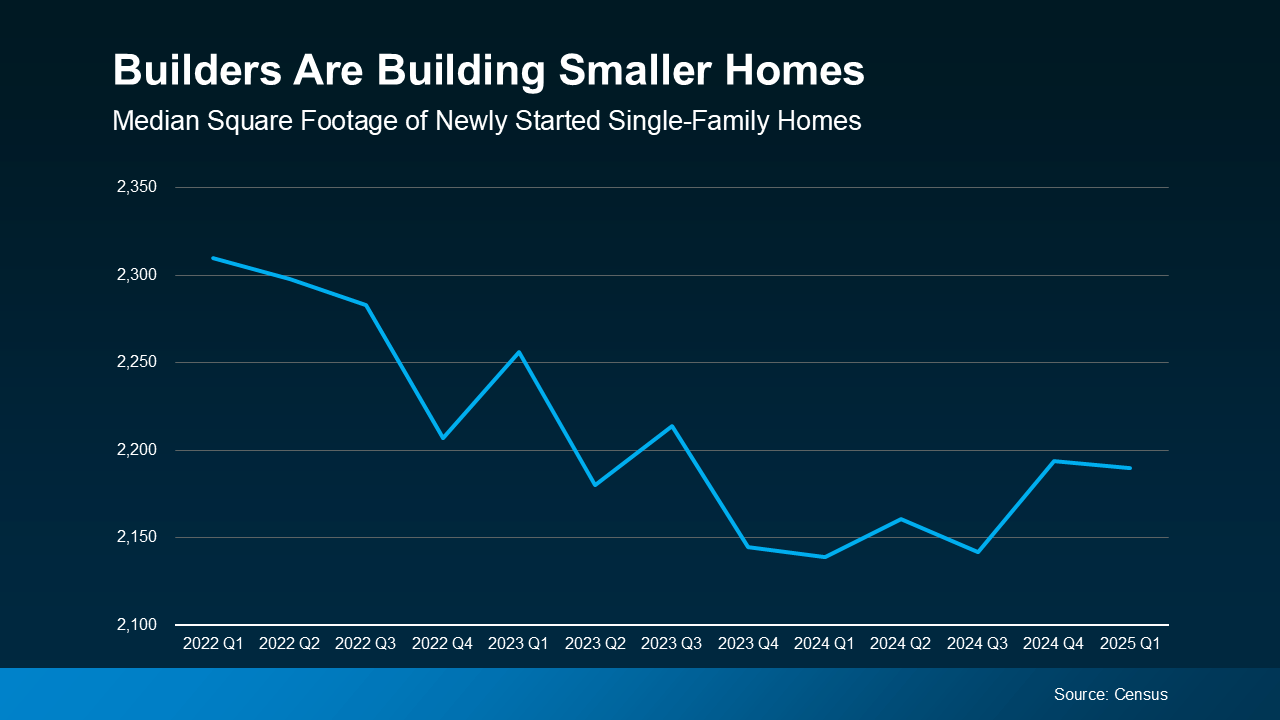

1. Builders Are Building Smaller Homes

Builders know that buyers are struggling with affordability today. So, instead of building big houses that may not sell, they’re building smaller ones that will. According to the Census, the average size of a newly built single-family home has dropped considerably over the past few years (see graph below):

And as size goes down, the price often does too. Smaller homes use fewer materials, which makes them less expensive to build. That helps builders keep prices lower so more people can afford them.

And as size goes down, the price often does too. Smaller homes use fewer materials, which makes them less expensive to build. That helps builders keep prices lower so more people can afford them.

2. Builders Are Offering Price Cuts and Incentives

In May, according to the National Association of Home Builders (NAHB), 34% of builders lowered their prices, with an average price drop of 5%. That’s because they want to be sure they’re selling the inventory they have before they build more.

On top of that, 61% of builders also offered sales incentives – like helping with closing costs or buying down your mortgage rate. These are all ways builders are making their homes more affordable, so these homes sell in today’s market.

Your Next Step? Ask Your Agent What’s Available Near You

If you’re trying to buy a home right now, be sure to talk to your agent to find out what builders are doing in and around your area. They can find new home communities, as well as builders who are offering incentives or discounts, and hidden gems you might not uncover on your own.

Plus, buying a newly built home often means there are different steps in the process than if you purchase a home that’s been lived in before. That’s why it’s so important to have your own agent who can explain the fine print. You want a pro in your corner to advocate for you, negotiate on your behalf, and make sure your best interests come first.

Bottom Line

You could get a home that’s brand new, with modern features, at a price that’s even lower than some older homes. Talk with a local real estate agent about what you’re looking for and see if a newly built home is the right fit for you.

If buying a home is on your to-do list, what would stop you from exploring newly built options?