Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

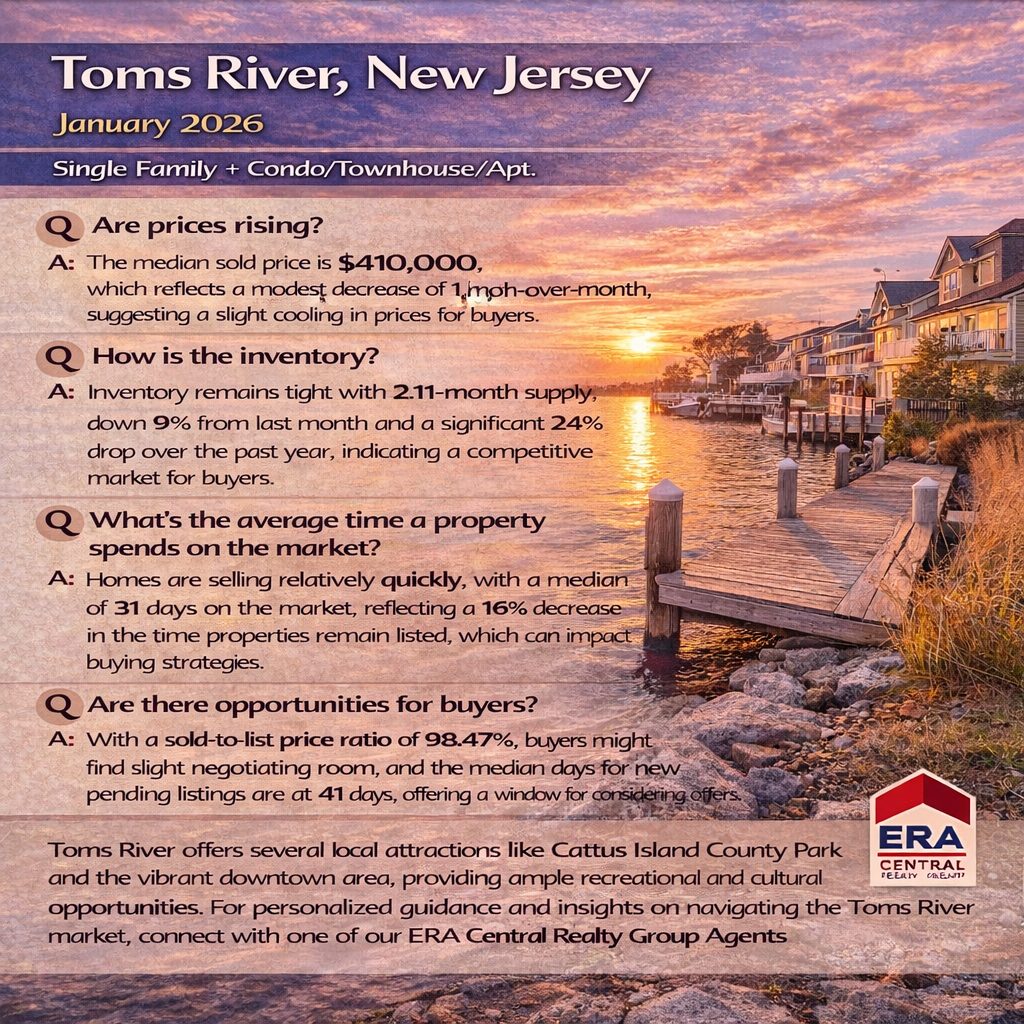

Toms River, New Jersey, January 2026, Single Family + Condo/Townhouse/Apt.

Q: Are prices rising?

A: The median sold price is $410,000, which reflects a modest decrease of 1% month-over-month, suggesting a slight cooling in prices for buyers.

Q: How is the inventory?

A: Inventory remains tight with a 2.11-month supply, down 9% from last month and a significant 24% drop over the past year, indicating a competitive market for buyers.

Q: What’s the average time a property spends on the market?

A: Homes are selling relatively quickly, with a median of 31 days on the market, reflecting a 16% decrease in the time properties remain listed, which can impact buying strategies.

Q: Are there opportunities for buyers?

A: With a sold-to-list price ratio of 98.47%, buyers might find slight negotiating room, and the median days for new pending listings are at 41 days, offering a window for considering offers.

Toms River offers several local attractions like Cattus Island County Park and the vibrant downtown area, providing ample recreational and cultural opportunities. For personalized guidance and insights on navigating the Toms River market, connect with one of our ERA Central Realty Group agents.