Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

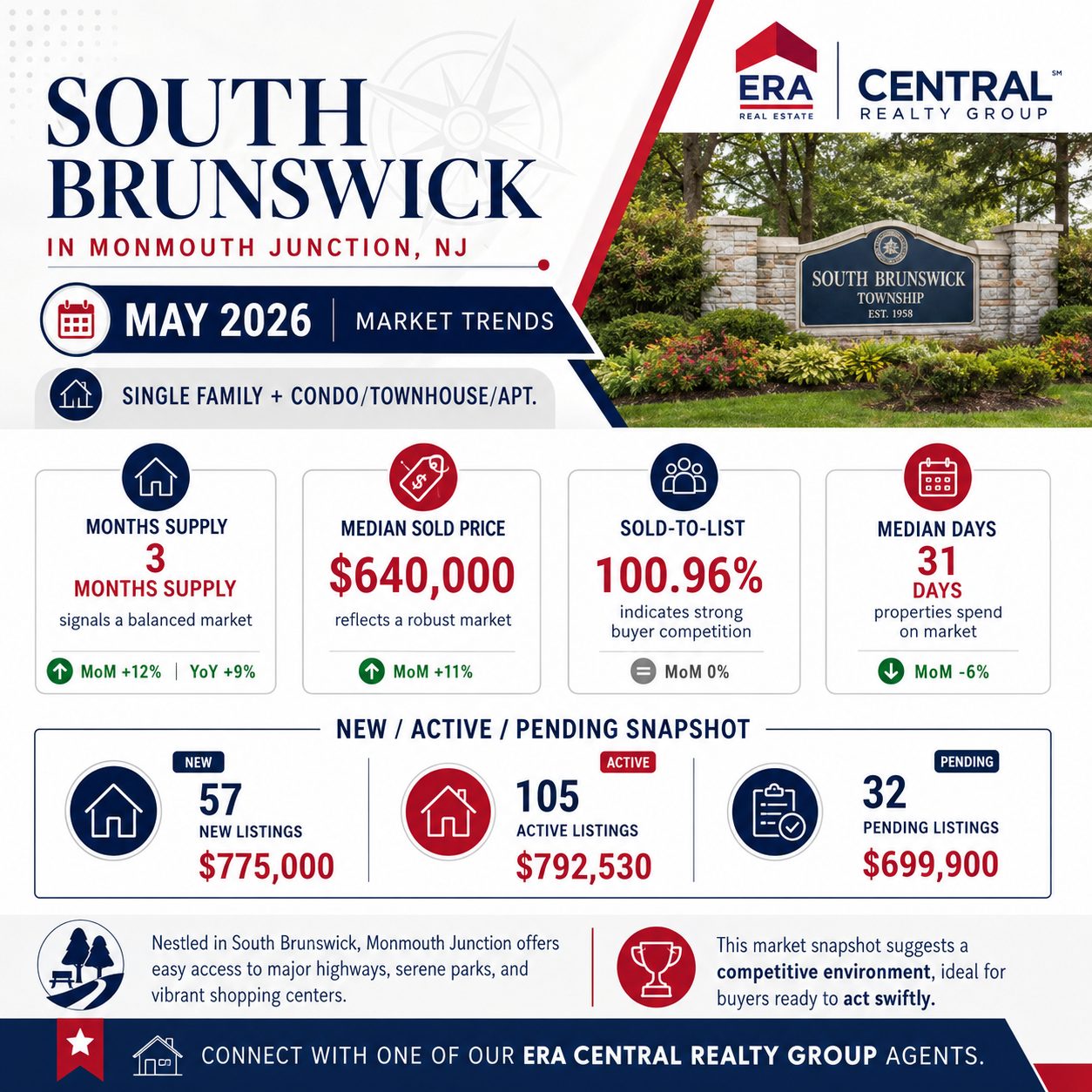

Spotlight on Spotswood, New Jersey, June 2026: Single Family + Condo/Townhouse/Apt.

Are prices rising?

Yes, the median sold price for homes in Spotswood is $560,000, reflecting a notable 32% month-over-month increase.

How’s the inventory looking?

The market currently has a three-month supply of inventory, with a 41% increase in inventory from the previous month, totaling 24 active listings.

What’s the median price for new listings?

The median list price for new listings is $489,900, while the median price for active listings is slightly higher at $507,500.

How long are homes staying on the market?

Homes are spending an average of 39 days in RPR, a significant 129% increase in market time compared to last month, offering buyers more time to consider their options.

Nestled near the Raritan River, Spotswood offers charming parks and convenient access to major highways for commuters. With a strong sold-to-list price ratio of 102.73%, buyers should be prepared for competitive offers. For personalized guidance on the Spotswood market, connect with one of our ERA Central Realty Group agents.